The United States Department of Defense has begun exploring plans to expand its strategic stockpile of critical minerals as part of a broader effort to strengthen supply chain resilience and secure materials essential for national security and advanced technologies. The Defense Logistics Agency (DLA), which manages the National Defense Stockpile, has issued requests for information regarding the potential procurement and storage of several key metals. The initiative reflects growing concern in Washington over the vulnerability of global supply chains and the increasing strategic importance of minerals used in defense systems, energy technologies, and advanced electronics.

The agency is seeking information related to five critical minerals: lithium, nickel, tin, chromium, and tellurium. Notices published by the Defense Logistics Agency call on potential suppliers and industry participants to provide details about available materials, product specifications, sourcing options, and current market conditions. The request also invites companies to outline their capacity to supply these metals and the potential availability of domestic or allied sources. Such consultations are often an early step before governments move forward with formal procurement programs designed to build or expand strategic reserves.

Lithium and nickel have become especially important in recent years due to their central role in battery production and energy storage technologies. These materials are widely used in electric vehicles, renewable energy systems, and various military applications that rely on advanced power systems. As global demand for batteries accelerates, competition for these minerals has intensified, prompting governments to prioritize access to reliable supply sources. By expanding its stockpile of these materials, the United States aims to reduce potential disruptions and ensure that critical industries can continue operating during periods of geopolitical or market instability.

Chromium and tin are also essential components in a range of industrial and defense applications. Chromium is widely used in the production of stainless steel and corrosion-resistant alloys, which are vital for military equipment, infrastructure, and aerospace technologies. Tin plays a crucial role in electronics manufacturing, particularly in solder used to connect electronic components on circuit boards. Tellurium, though less widely known, is a strategic mineral used in advanced semiconductors, solar energy technologies, and certain specialized defense systems. Together, these materials form an important foundation for modern industrial and military capabilities.

The move comes at a time when governments around the world are increasingly concerned about supply chain security and the concentration of critical mineral production in a limited number of countries. Many key minerals are mined or processed in regions that may be subject to geopolitical tensions, trade restrictions, or environmental challenges. These risks have prompted policymakers to explore strategies that include diversifying supply sources, encouraging domestic production, and building national reserves to cushion potential supply shocks.

Expanding the National Defense Stockpile would provide the United States with a buffer against market volatility and geopolitical disruptions. Strategic reserves allow governments to maintain access to essential materials even if international supply chains are interrupted. Analysts note that such measures are becoming increasingly common as global competition for critical resources intensifies and countries seek to secure the materials needed for emerging technologies and national defense capabilities.

Budget4 months ago

Budget4 months ago

Latest News4 months ago

Latest News4 months ago

Latest News4 months ago

Latest News4 months ago

Latest News4 months ago

Latest News4 months ago

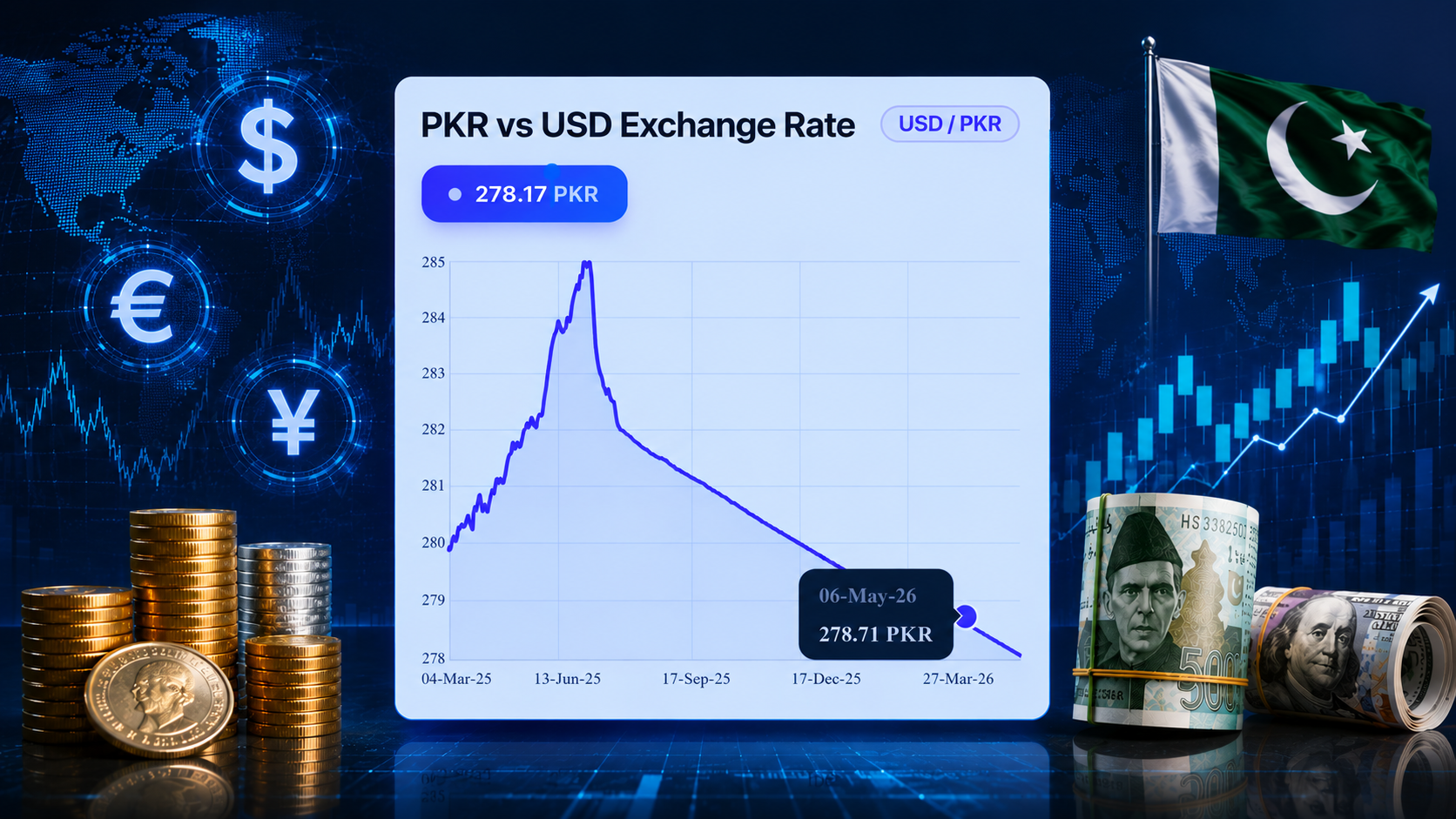

Currencies4 months ago

Currencies4 months ago